ganda ended the last fiscal year with $5.8 billion in declared gold exports — a figure that reads like a headline and spends like a warning. Volume is rising faster than the documentary infrastructure that is supposed to accompany it. That gap is where risk lives, and it is the single most useful thing a procurement desk in Zurich or Singapore can understand about Kampala right now.

This note is written for the buyer who already knows the press releases. It covers the three shifts we expect to see reshape institutional sourcing through the rest of 2026, what each shift means in practical terms at the desk level, and where we think the compliance surface is moving next.

01

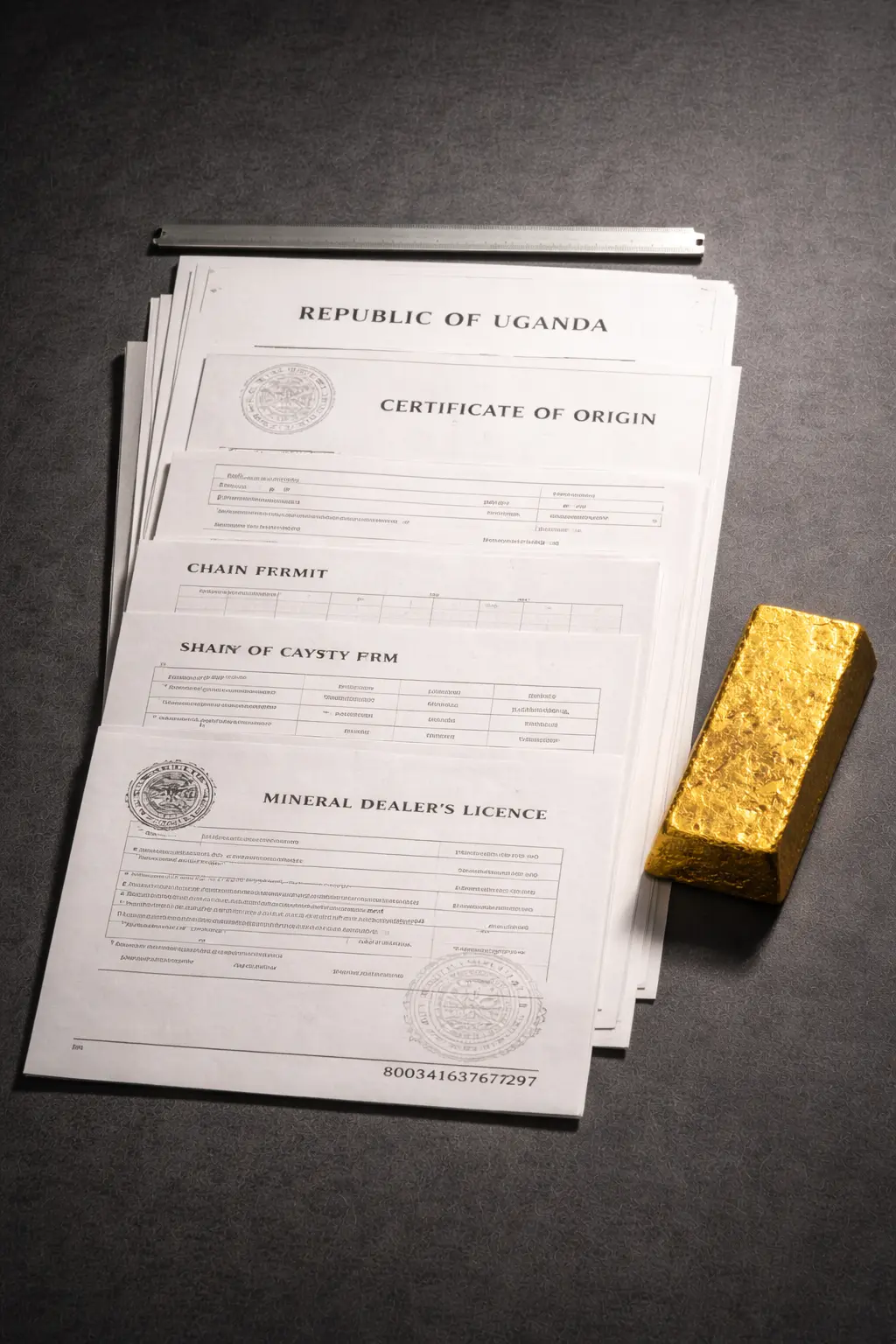

The headline number hides a documentary gap.

A $5.8B export year is not, on its own, a quality signal. Uganda is a crossroads for regional gold — ore and semi-refined material flow in from four neighbours and leave through a single pair of declared exit corridors. Most of the volume growth over the past eighteen months came from material that was not extracted inside Uganda's own concession boundaries.

For a buyer whose compliance programme is built around OECD due-diligence expectations, that distinction is not a footnote. It is the first question. "Where was the metal actually mined?" And the second: "Who signed for it the day it crossed the border?" The country of export is the easy answer. The country of origin is the one that earns the certificate.

$5.8B

Declared gold exports

Uganda, last fiscal year

≈37%

Originating in-country

Our desk estimate

4

Neighbour source flows

DRC, Tanzania, South Sudan, Rwanda

02

The Mineral Value Addition Policy changes what leaves the country.

The Mineral Value Addition Policy — in effect since the start of this year — is written around a single premise: Uganda should retain more of the processing work before material is exported. In practice, that means more doré is going to be assayed, refined, or semi-refined inside Uganda before it is cleared for export. That is a substantive change for any buyer used to receiving unprocessed material and refining it downstream.

The policy is being read in three different ways by three different camps. The regulators read it as an industrial development lever. The large exporters read it as a cost shift that will compress margins. We read it as a compliance accelerator: the more processing that happens inside a jurisdiction with an improving assay and custody regime, the more defensible the paper trail becomes.

“The signatures that matter are the ones written before the metal crosses the border, not after. The policy is pulling the signatures closer to the seam.”

— Internal desk memo, Al Areen Trade

03

Where the compliance surface is moving next.

Two regulatory conversations are worth watching in the back half of 2026. The first is a proposed tightening of the export licensing protocol that would require each exporter to file a declared source concession for every declared kilo — a move from company-level to material-level attestation. The second is an early draft of a regional chain-of-custody standard being circulated between the Ugandan, Tanzanian, and Kenyan mining ministries.

- 01Material-level attestation on export licences — a shift from company-level to kilo-level reporting.

- 02Regional chain-of-custody draft circulating between three mining ministries.

- 03Audit appointments at the two largest regional refineries, first made public last month.

- 04Proposed bullion vault licensing framework — the first attempt at a domestic custody regime.

Buyers who wait for the final regulatory language before adjusting their sourcing will be adjusting from behind. The direction is legible now: more documentation per kilo, closer to the seam, signed by named people. The suppliers who already work that way will spend the next six months running the same playbook, a little louder.